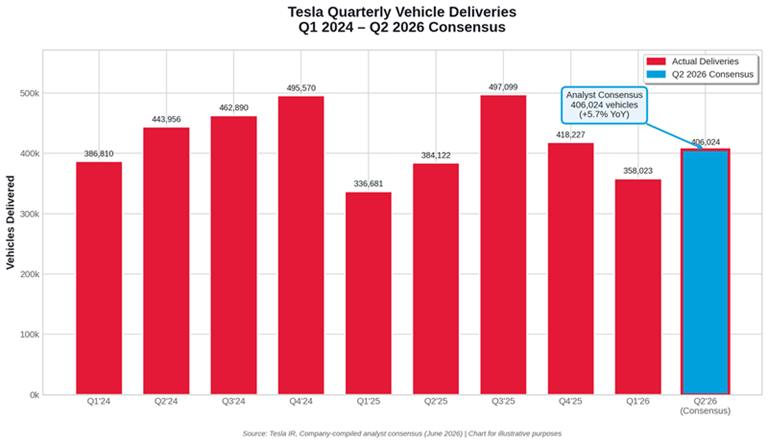

Tesla just released its latest company-compiled analyst consensus for Q2 2026 deliveries, and the headline figure is 406,024 vehicles. That’s up modestly from the 384,122 delivered in Q2 2025 — roughly 5.7% growth.

On the surface, it looks like a quiet rebound after Q1’s softer numbers. But dig a little deeper, and this consensus reveals a company navigating a delicate balance: steadying vehicle volumes while its energy business quietly accelerates, all while analysts remain cautious after last quarter’s inventory buildup.

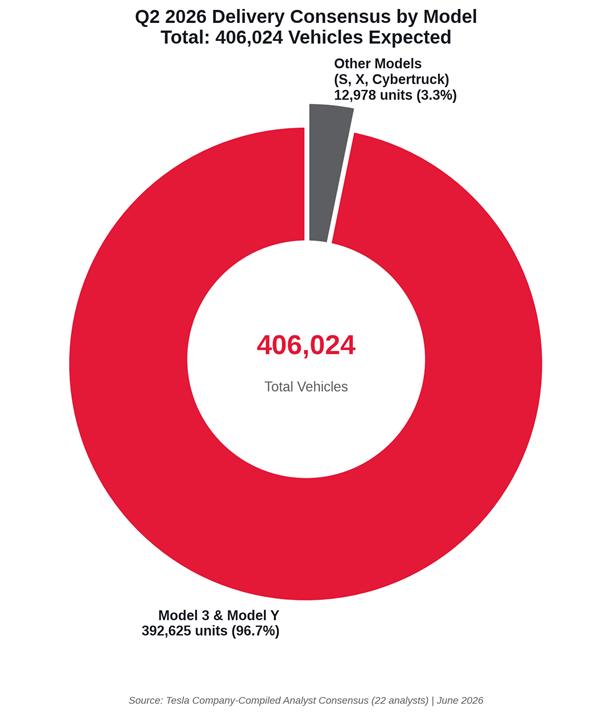

According to the consensus compiled from 22 sell-side analysts (including heavyweights like Goldman Sachs, Morgan Stanley, and JPMorgan), the split is heavily skewed toward Tesla’s volume kings:

- Model 3/Y: 392,625 deliveries expected

- Other models (Model S, Model X, and Cybertruck): 12,978 deliveries

That “other models” figure is actually a slight step down from the 16,130 delivered in Q1 2026.

The median estimate sits a touch higher at 408,609, with a standard deviation of about 15,000 vehicles. In other words, most analysts are clustered in a fairly narrow band around 400k–420k.

For context, Q1 2026 actual deliveries came in at 358,023 vehicles against a consensus of roughly 365,645 — a miss that left Tesla with over 50,000 extra vehicles in inventory.

Q1’s Inventory Shadow Still Lingers

That inventory overhang matters more than most headlines admit. Tesla produced 408,386 vehicles in Q1 but only delivered 358,023. The gap wasn’t catastrophic, but it does mean production discipline will be key in Q2.

If demand is tracking as Goldman Sachs believes — the bank recently raised its own Q2 forecast to 420,000, citing stronger sales data out of the U.S., China, and Europe — then Tesla could draw down some of that inventory and still post a clean beat.

If demand is merely “okay,” we could see another quarter of production running slightly ahead of deliveries. Either way, the 406k consensus feels achievable rather than ambitious.

One detail that hasn’t gotten much attention is the expected dip in higher-margin and newer vehicles. The consensus calls for fewer than 13,000 “other model” deliveries in Q2 versus 16,130 in Q1.

Cybertruck production continues at the Austin Gigafactory, and while it remains a distinctive presence on American roads, it hasn’t yet become a high-volume product. Model S and X sales have long been niche. This modest pullback in the consensus may simply reflect normal quarterly variation — or it could hint that Tesla is prioritizing throughput on the Model 3/Y lines while newer programs (including any refreshed or lower-cost vehicles) are still ramping.

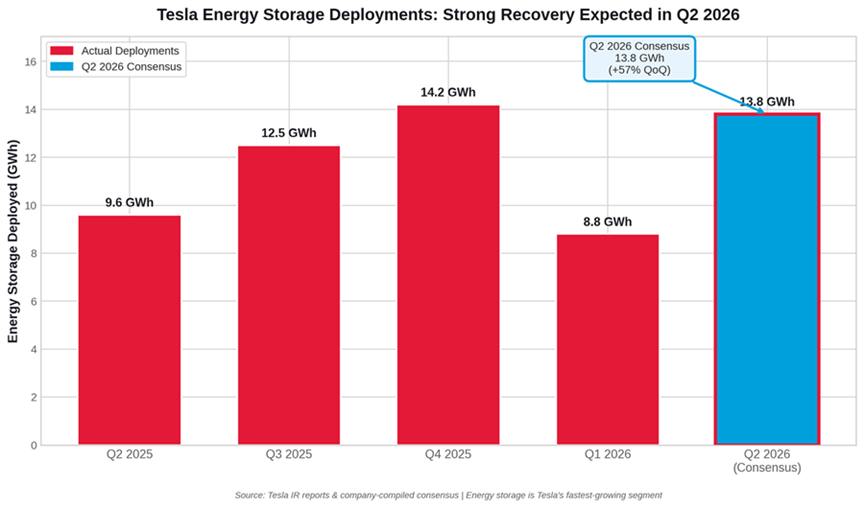

Energy Storage Is the Real Growth Story

While vehicle deliveries are expected to grow modestly, Tesla’s energy storage deployments are projected to jump sharply to 13.8 GWh in Q2 2026 — up from just 8.8 GWh in Q1.

That’s nearly matching the strong Q4 2025 level and represents one of the clearest growth vectors in Tesla’s entire business right now. Energy storage has become less “lumpy” in the eyes of some analysts and more of a reliable, high-margin complement to the automotive side.

For U.S. readers, this matters. Megapack deployments support grid stability, data center power needs, and utility-scale projects across states that are aggressively building out renewables. It’s also a business less exposed to the whims of EV incentive policy or consumer financing rates.

For U.S. Tesla owners and prospective buyers, the 406k figure suggests the company is stabilizing volume without dramatic growth — at least in the near term. The core Model 3 and Model Y lineup continues to do the heavy lifting, which is good news for parts availability, service capacity, and resale values.

For investors, the consensus sets a clear, measurable bar that Tesla itself published. Historically, these self-compiled numbers have sometimes been conservative, but Tesla did miss the Q1 bar. A clean beat or in-line result in early July would likely be viewed positively, especially if accompanied by commentary on inventory normalization and energy momentum.

Longer-term, the full-year 2026 consensus sits around 1.65–1.67 million vehicles — essentially flat compared with 2025. That’s a far cry from Tesla’s 2023 peak and underscores why the stock’s valuation increasingly hinges on autonomy, robotaxi, and new vehicle programs rather than pure volume growth.

Tesla typically releases official Q2 production and delivery numbers in the first few days of July. That report will show whether the company matched, beat, or fell short of this 406k consensus — and, just as importantly, how production compared with deliveries.

Goldman Sachs thinks the number could come in higher. Many other analysts are playing it safer after Q1’s inventory build. The truth is probably somewhere in between.

What’s clear is that Tesla is no longer the hyper-growth EV story it once was. Instead, it’s a more mature automaker with a rapidly expanding energy business and a portfolio of ambitious future bets. The 406,000-vehicle consensus for Q2 2026 is less a victory lap and more a progress report — one that shows the company still has work to do on the volume side while its other engines are starting to hum louder.

For American drivers watching the EV transition, for investors holding TSLA, and for anyone interested in where Tesla goes next, the next few weeks should bring useful clarity. The number itself is just the starting point.

Related Post