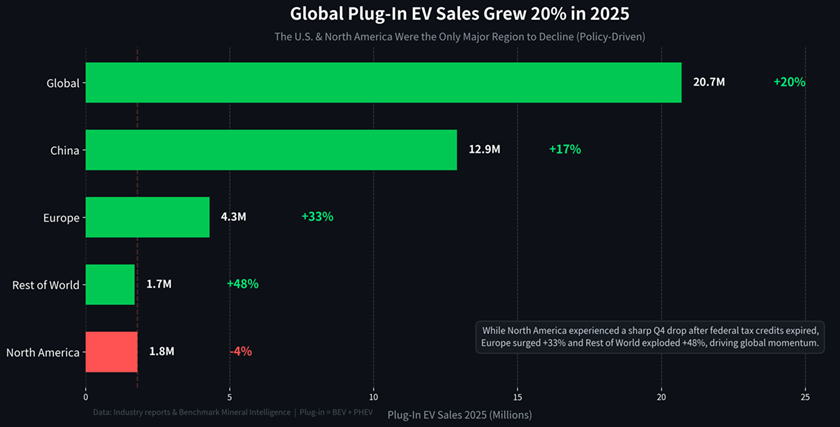

EV demand collapsing in America, tax credits vanishing, buyers fleeing. Yet step back from the U.S. noise and the numbers tell a very different story. In 2025, the world bought roughly 20.7 million plug-in electric cars—battery-electric vehicles and plug-in hybrids combined—up 20% from 2024.

That is not a slowdown. That is the strongest full-year growth the category has seen in a maturing market. The real question for American readers is not whether plug-ins are fading, but why the United States became the glaring exception while almost everywhere else accelerated.

U.S. Numbers Look Messy

Domestic plug-in sales landed around 1.5 million units in 2025, down about 4% from the prior year. Battery-electric vehicles made up the large majority, but the story was dominated by extreme quarterly swings rather than any organic rejection of the technology.

Q3 was a record: nearly 438,000 EVs sold as buyers rushed to capture the federal clean vehicle tax credit before it expired at the end of September. Market share hit an all-time high of 10.5%. Then Q4 collapsed to roughly 234,000 units and a 5.7% share once the incentive disappeared and policy uncertainty took over.

The full-year result was still respectable—electrified vehicles of all kinds (including strong hybrids) reached 22% of total U.S. light-duty sales, up from 20% in 2024. But the headline “slowdown” narrative stuck because it fit a convenient political storyline. The underlying data show something narrower: an artificial demand spike followed by a policy-induced hangover, not a broad consumer turn against plug-ins.

- Europe surged 33% to 4.3 million plug-ins, with both pure EVs (+31%) and PHEVs (+38%) contributing.

- China added another 12.9 million units (+17%), still the volume engine of the industry.

- Rest of World exploded 48% to 1.7 million units, fueled largely by affordable Chinese models landing in Latin America, Southeast Asia, and other emerging markets.

PHEVs played an outsized role in Europe’s growth, offering drivers a practical bridge: electric for daily commutes, gasoline for long trips, and lower upfront cost than many full EVs. That same flexibility is winning converts in markets where charging infrastructure is still patchy. The lesson is not that Americans hate electric cars; it is that many buyers—here and abroad—want options that reduce risk while still cutting fuel use and emissions.

Global scale is already bending the cost curve in our favor. Every additional million plug-ins sold worldwide helps drive battery prices lower, improves supply chains, and funds the next generation of chemistries and manufacturing. U.S. gigafactories and suppliers benefit even when domestic retail sales wobble, because volume anywhere improves economics everywhere.

More models are coming. Legacy automakers that stumbled early are now moving real metal: GM’s EV volume jumped sharply in 2025 on the back of Equinox EV, Blazer EV, and others. Ford’s Mustang Mach-E and F-150 Lightning carved out loyal followings. The product gap that existed in 2022–2023 has narrowed dramatically. When prices and real-world utility line up, American buyers respond—as the Q3 rush proved.

The policy whiplash also carries a strategic warning. Abrupt incentive changes create exactly the volatility we saw in late 2025. Stable, predictable rules—whether through targeted credits, infrastructure spending, or performance standards—let manufacturers and buyers plan. The countries and regions that maintained clearer long-term signals captured the 20% growth. The U.S. can still decide which lane it wants to be in.

2026 will almost certainly be another transitional year at home. Without the federal credit, some price-sensitive segments will feel the absence. Yet the fundamentals that drove global growth—falling battery costs, more capable and affordable vehicles, PHEVs as a pragmatic on-ramp, and expanding charging networks—are not reversing. They are simply arriving at different speeds in different places.

For U.S. consumers, the practical takeaway is straightforward: the best time to buy a plug-in is when the specific vehicle meets your needs on range, price, and charging access. Those vehicles exist today in greater numbers and at better value than they did even two years ago. The global 20% surge is proof that millions of drivers in wildly different circumstances have already made that calculation and said yes.

The slowdown narrative was always too narrow. The real story is that plug-in cars kept winning—everywhere except where policy deliberately threw sand in the gears. That is a very different, and ultimately more encouraging, headline for anyone thinking about what they will drive next.

Related Post