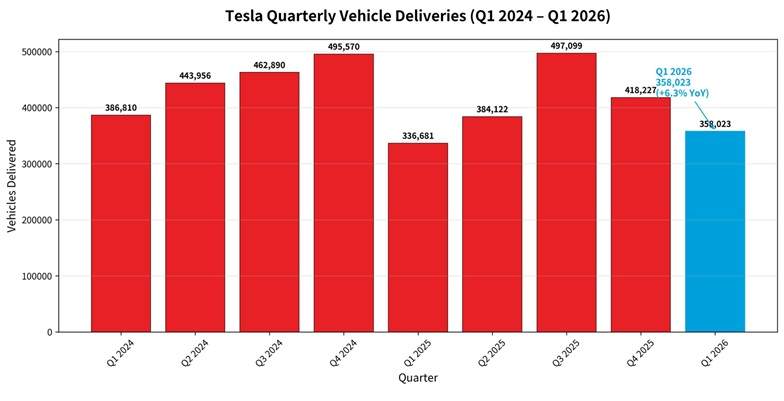

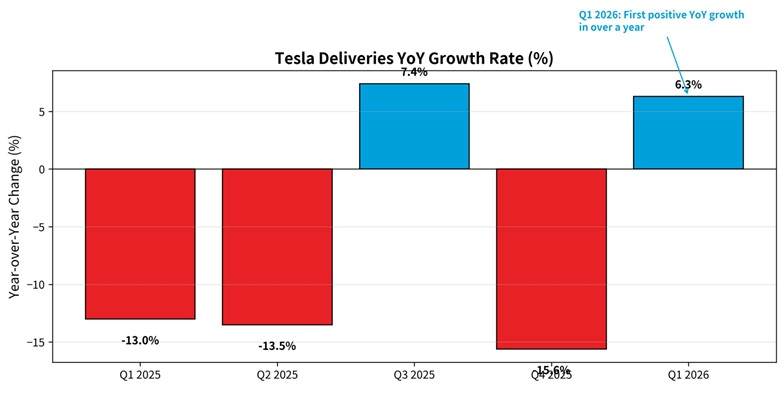

Tesla reported 358,023 vehicle deliveries in the first quarter of 2026, a modest 6.3% year-over-year increase from 336,681 units in Q1 2025. Production reached 408,386 vehicles, up 13% from the prior year. Model 3 and Model Y continued to dominate, while other models — primarily the Cybertruck — saw deliveries jump 25% year-over-year. Global inventory stood at 27 days of supply.

On the surface, these figures look like steady but unspectacular progress in a competitive EV market. Dig deeper into Tesla’s own Q1 2026 Update and earnings commentary, however, and a different narrative emerges: these deliveries are not the main event. They are the byproduct of a company deliberately shifting capital, factory lines, and supply chains toward the infrastructure required for unsupervised autonomy at scale.

Demand Rebound Meets Strategic Restraint

Tesla noted continued growth in APAC and South America alongside a clear rebound in both North America and EMEA. This regional recovery happened even as the company maintained pricing discipline on higher trims of the Model Y in May — the first increase in roughly two years on Premium and Performance variants. The 27 days of inventory is not a sign of softening demand; it reflects deliberate production pacing ahead of the Cybercab transition.

Tesla stated explicitly in its Q1 materials that the Cybercab “will begin to replace the existing Model Y fleet and will be the largest volume vehicle in the fleet over time.” Maintaining lean but healthy inventory now preserves flexibility for that fleet rotation rather than flooding dealers with vehicles that may soon share roads with purpose-built robotaxis.

The 25% growth in “other models” deliveries — driven largely by Cybertruck — further undercuts narratives that the vehicle is a niche curiosity. Production is scaling, international deliveries (including the UAE) have begun, and the truck remains the primary early user of Tesla’s 4680 cells.

Battery Vertical Integration

The most under-discussed element in Q1 reporting is how Tesla is using current production to fund and de-risk its own battery supply for the autonomy era. In the official update, the company detailed active ramps:

- Texas 4680 production now at 40 GWh capacity (in production phase)

- Texas cathode materials at 10 GWh (early ramp)

- Texas lithium refining at 30 GWh (early ramp)

- Nevada LFP at 7 GWh (early ramp)

These are not pilot numbers. They represent concrete vertical integration progress that reduces reliance on external suppliers precisely as trade barriers and tariff risks rise. The same update notes Tesla has begun producing certain Model Y battery packs with in-house 4680 cells again, “unlocking an additional vector of supply.”

This matters because the Cybercab and future high-volume autonomous platforms will need cost-effective, domestically or regionally sourced cells at massive scale. The current Model 3/Y and Cybertruck volumes are effectively stress-testing and subsidizing that supply chain before robotaxi volumes arrive.

Tesla spent $2.5 billion in capex during Q1 alone and deployed an additional $2.0 billion into SpaceX equity. Cash and short-term investments rose to $44.7 billion. The company is simultaneously ramping AI compute (Cortex 1 and 2 in Texas), preparing Optimus production lines (Fremont targeting 1 million robots annually; Texas for a long-term 10 million unit capacity), and building the new Megafactory in Texas for Megapack 3 production later this year.

These are not distractions from the auto business. They are the infrastructure layer required for the autonomy business model Tesla has described: a fleet where Cybercabs generate high-utilization revenue and owners can eventually enroll personal vehicles in the network.

Unsupervised Robotaxi operations expanded in April to Dallas and Houston (Austin already ramping), with cumulative paid miles reaching 1.8 million. Preparations are underway for additional major metros. The earnings call reinforced that initial Cybercab production will follow an S-curve — slow at first, then exponential — with volume production targeted for 2026.

In a traditional automaker, rising inventory often signals trouble. At Tesla right now, it signals preparation. The company is deliberately building the manufacturing, battery, AI compute, and regulatory runway for a vehicle (Cybercab) that has no steering wheel or pedals in its primary configuration and is designed from the ground up for high-utilization robotaxi economics.

The 358,023 deliveries and 27 days of supply are the visible output of factories that are already being retooled — literally and figuratively — for the next phase. Model Y lines will eventually yield capacity to Cybercab. 4680 production that today supports Cybertruck and select Model Y variants is scaling for the vehicles that will dominate the fleet “over time.”

Tesla’s Q1 results show an automaker that has stopped optimizing solely for quarterly vehicle volume and has begun optimizing for the capital intensity and supply chain resilience required for unsupervised autonomy at fleet scale. The modest delivery growth, the Cybertruck volume increase, the lean inventory, and the aggressive battery and AI investments all point in the same direction.

The numbers everyone quotes — 358,023 deliveries, 6.3% growth, 27 days inventory — are accurate. They are also incomplete. The real story of Q1 2026 is the quiet, expensive, and deliberate construction of the foundation on which Tesla intends to build the largest autonomous fleet the world has seen.

That work is already underway in Texas, Nevada, and across regulatory desks from the Netherlands to China. The vehicles delivered in Q1 were simply the ones still needed while that foundation is poured.

Related Post